VA Loan Partial Entitlement Explained

Alright, so you already know you can use your VA loan again.

But now you pull your Certificate of Eligibility, start looking at homes, and something doesn’t make sense.

When you start talking to your lender about numbers, it looks like you might need a down payment. But why?

This is an extremely common situation military buyers run into.

Nothing is wrong. This is normal. You just need to understand how your buying power works on your second VA loan.

How VA Loan Entitlement Actually Works

The Department of Veterans Affairs does not lend you money with a VA Loan. Instead, it guarantees 25 percent of the loan to the lender, similar to an insurance policy. That guarantee matters because it reduces the lender’s risk.

If a borrower ever defaults, the VA steps in and covers a portion of the loss. From the bank’s perspective, that makes the loan significantly less risky compared to a standard mortgage. And when risk goes down, lenders are more willing to offer better terms.

That’s what allows you to buy with little to no money down, secure more favorable interest rates, and avoid monthly mortgage insurance.

But that backing isn’t unlimited.

If you’ve used the VA Loan once before, part of it is already tied up in another home. Meaning, you simply have less available for your next purchase.

And that’s what creates the question:

👉 How much home can I afford with what I have left?

Understanding Your Loan Limit in 2026

The easiest way to understand your buying power is to start with the loan limit in your area.

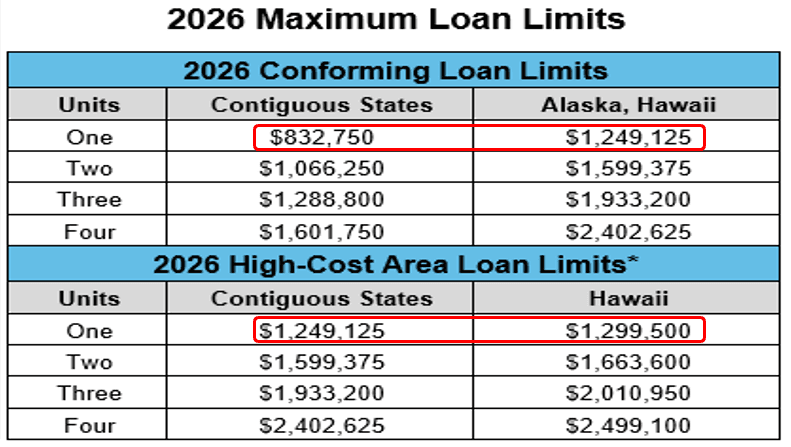

If you look at Figure 1 below, you’ll see two sets of loan limits. There is a standard limit that applies to most of the country, and a higher limit that applies to more expensive areas.

Figure 1: 2026 Maximum Loan Limits

For example, in 2026:

- Standard one-unit limit: $832,750

- High-cost one-unit limit: $1,249,125

That number is what your VA benefit is built on.

And this is important. Even if you are buying a duplex, triplex, or fourplex, the VA still uses the one-unit loan limit when calculating your available buying power for a second purchase.

The higher multi-unit limits you see in the chart do not apply to VA Loans.

Standard Marine Corps counties limits include: Camp Lejeune, MCAS New River, MCAS Cherry Point, MCRD Parris Island, MCAS Beaufort, MCAGCC Twenty-nine Palms, MCB Barstow, MCAS Yuma, and MCB Albany

High-cost Marine Corps counties limits include: The National Capital Region, MCB Quantico, MCAS Miramar, Camp Pendleton, MCRD San Diego, and MCB Hawaii

If you want to check it yourself, you can use the official county-by-county loan limit list from the Federal Housing Finance Agency.

How to Calculate Your Remaining VA Buying Power

If you still have an existing VA loan on another property, part of your buying power is already being used.

And this is important.

Your entitlement is based on the original loan amount, not your current balance.

Even if you’ve paid the loan down, that portion of your VA benefit is still tied up until the loan is paid off or the home is sold.

A simple way to estimate what you have left is to take the loan limit in your area and subtract your original VA loan amount.

What you’re left with is roughly how much you can borrow again using your VA loan without needing a down payment.

When You’ll Need a Down Payment

At this point, it becomes very straightforward.

- Step 1: Max Loan Limit – Original Loan Amount = Max Purchase Price

- Step 2: Future Purchase Price – Max Purchase Price = Amount Over Zero-Down Limit

- Step 3: Amount Over Zero-Down Limit ÷ 4 = Required Down Payment

That gives you the amount you need to bring to closing if you go above your zero-down buying power.

VA Loan Partial Entitlement Example (Step-by-Step)

Let’s walk through this cleanly.

Start with the standard loan limit of $832,750.

Now assume your existing original VA loan on your rental property was $500,000.

Step 1: Find your zero-down buying power

- $832,750 – $500,000 = $332,750

- 👉 That means you can buy up to $332,750 with zero down

Step 2: What happens if you go above that?

- Now let’s say the home you want is $400,000.

- $400,000 – $332,750 =$67,250

- 👉 You are $67,250 over your zero-down limit.

Step 3: Calculate your down payment

- $67,250 ÷ 4 = $16,812.50

- 👉 That means your required down payment is about $16,813

When to Consider Other Loan Options

At this point, you know your numbers.

If your down payment starts getting higher, it’s worth taking a step back and comparing your options.

In some cases, a conventional or FHA loan may require less cash upfront than a VA loan with partial entitlement.

For a full breakdown, check out our guide on Loan Options for Military Buyers.

Final Thoughts on Using Your VA Loan Again

If this is the first time you are running into this, it can feel like the numbers suddenly stopped working.

They didn’t.

You just moved from the simple version of the VA loan into a more complex situation, where it may or may not be the best option anymore.

Once you understand how to calculate your buying power and what happens when you go above it, the path forward becomes clear.

You are not stuck. You just need to understand your numbers and build a plan around them.