Which Loan Strategy Makes More Sense for Military Homebuyers?

One of the most common strategy conversations I have with my military buyers is whether they should choose a fixed-rate VA loan or a VA adjustable-rate mortgage (ARM).

At first glance, the answer seems simple: a fixed-rate loan offers long-term stability, while an ARM offers a lower payment upfront.

But for military buyers, this decision is often more strategic than that.

Unlike many civilian buyers, military families often know there is a realistic chance they may PCS within the next three to five years. That shorter ownership timeline can make a lower introductory rate attractive. At the same time, many military buyers eventually turn their homes into rental properties or long-term investments.

That means this decision is about balancing short-term savings, long-term cash flow, flexibility, and risk. Choosing the wrong loan could cost you thousands in unnecessary payments or create future cash flow problems if your plans change.

What Is a Fixed Rate VA Loan?

A fixed-rate VA loan means your interest rate stays the same for the life of the loan. Your principal and interest payment remains stable, though taxes and insurance may change over time.

This is the most common option because it removes uncertainty. For buyers planning to stay long term or keep the property as a rental later, that predictability can make budgeting and long-term cash flow planning easier.

Benefits of a Fixed Rate VA Loan

✔ Predictable monthly payment

✔ Easier long-term budgeting

✔ No risk of future interest rate increases

✔ Better for long-term ownership

✔ Easier to plan for future rental cash flow

Downsides of a Fixed-Rate Loan

✘ Higher starting interest rate than an ARM

✘ Higher monthly payment upfront

✘ Less immediate buying power

What Is a VA ARM?

A VA ARM is an adjustable-rate mortgage. Many lenders will offer different terms, such as 3/1, 3/5, 5/5, 7/1, or 10/1 ARMs. The “5/1” means the rate is fixed for the first five years and adjusts once per year after that based on market conditions and the terms of the loan.

Because lenders are taking less long-term rate risk, the starting interest rate is usually lower. That lower rate reduces the monthly payment during the fixed period.

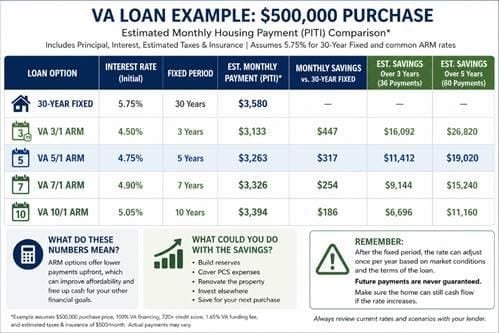

How Much Can You Save with a VA 5/1 ARM?

Let’s compare a real-world example:

In this example, the VA 5/1 ARM saves approximately $317 per month compared to the 30-year fixed-rate option.

When a VA ARM Makes Sense

A VA ARM tends to make the most sense when the ownership timeline is shorter.

If you expect to sell or potentially refinance before the first adjustment period, you may be able to capture the lower payment without taking on much long-term risk.

A lower payment can also increase your purchasing power, allowing you to qualify for a more expensive home, stay comfortably within your BAH budget, or buy in a better location with stronger long-term resale or rental potential.

Another factor to consider is that your income may increase over time. Over the next several years, you may receive promotions, time-in-service raises, annual military pay increases, or higher BAH, which can make future payment increases easier to absorb if you keep the home longer than expected.

A VA ARM may also make sense if you want to preserve cash reserves for upcoming expenses, renovations, repairs, or future investments.

In these situations, the VA ARM can be a smart short-term financial tool.

The Risks of a VA ARM

The biggest risk is payment shock.

After year five, the interest rate can adjust based on market conditions and the terms of the loan. While that can mean a lower payment if rates fall, buyers should plan conservatively because rates can also rise.

It is important to know that many ARMs have “caps,” which are limits on how much the interest rate can increase. These caps typically limit how much the rate can rise at the first adjustment, how much it can increase each year after that, and the maximum increase over the life of the loan.

For example, some ARMs may have 1/1/5 caps. That means the rate may increase by up to 1% at the first adjustment, up to 1% per year after that, and no more than 5% above the original rate over the life of the loan.

Understanding these caps can help buyers estimate worst-case future payments before choosing the loan.

That matters if your plans change.

A property that cash flows comfortably today may stop cash flowing if the ARM adjusts and rents do not rise at the same pace. The lower payment today can create future financial stress if you decide to keep the property longer than expected.

Another major mistake buyers make is assuming they can simply refinance later.

Refinancing is never guaranteed. It depends on your credit, income, debt ratios, home value, and future interest rates.

For buyers who expect to sell before the first adjustment, this risk may be minimal. But for buyers who may keep the property long term, understanding the downside matters just as much as understanding the savings.

When a Fixed Rate VA Loan Is Better

A fixed-rate loan is usually stronger when stability matters more than short-term savings.

This often applies when you may keep the home as a rental because stable payments make long-term cash flow easier to predict.

It may also make more sense if you are unsure of your timeline, are buying near your budget limit, or simply prefer certainty over flexibility.

For many buyers, peace of mind is worth paying more today.

Think Like an Investor Before Choosing

Before choosing between a fixed loan and an ARM, ask yourself:

- How long do I realistically plan to own this home?

- Would I rent it out or sell if I PCS?

- Can I afford the payment if rates increase?

- Do I prefer stability or lower upfront costs?

- How much would I actually save?

Savvy buyers think beyond the monthly payment and consider their exit strategies before purchasing a home. If life or the market changes, can you sell for a profit, rent for positive cash flow, or refinance if rates improve later? And if the market softens, could you at least break even long enough to wait for a better time to sell? The more flexibility a property gives you, the less risky and more strategic the purchase becomes.

Bottom Line: Which VA Loan Is Better?

Neither loan is automatically better. The right choice depends on your timeline, your cash reserves, your long-term investment goals, and your tolerance for risk.

If this is a short-term tactical purchase, a VA ARM may maximize short-term savings and preserve cash.

If this property is part of a long-term investment strategy, a fixed-rate VA loan may better protect long-term cash flow and reduce risk.

If you’re military and considering buying, reach out anytime. I’d be happy to help you compare your options and decide which strategy makes the most sense for your goals.